Do you struggle to find DMEPOS coverage for clients with lower credit scores? Big "I" Markets partner Goldleaf can help.

If your insured has an unsatisfactory credit history report or unfavorable financials, Goldleaf underwriters' experience and access to many surety markets allows them to place bonds when others may not be able to.

What is a DMEPOS Bond?

Medicare Bonds, often referred to as DMEPOS Bonds, are mandatory for manufacturers and suppliers of durable medical equipment, prosthetics, orthotics and supplies (DMEPOS). The Centers for Medicare & Medicaid Services (CMS) published a final rule titled, "Medicare Program: Surety Bond Requirement for Suppliers of Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS)" in the Federal Register on January 2, 2009. This final rule implemented Section 4312(a) of the Balanced Budget Act of 1997 and requires certain DMEPOS suppliers to obtain and maintain a surety bond on continuing basis. This surety bond aims to prevent fraudulent activity within the industry.

What is the bond amount?

Section 4312(b) requires that a surety bond be in the amount of not be less than $50,000. Most suppliers are required to obtain a $50,000 surety bond. However there are several exceptions.

-

The bond amount will increase beyond the $50,000 for suppliers who are deemed high risk.

-

Suppliers with multiple locations are required to obtain a bond for each National Provider Identifier (NPI). For example, a larger DMEPOS supplier with 20 practice locations would be required to secure a $1 million Medicare (DMEPOS) Bond, one for each location.

Who is exempt?

Suppliers who are exempt from the bonding requirement include:

-

Government-owned suppliers that have provided CMS with comparable surety bond under state law. The surety bond shall state that CMS is an obligee and cover obligations concerning claims

-

State-licensed orthotic and prosthetic personnel in private practice making custom orthotics and prosthetics if the business is solely-owned and operated by said personnel and is billing only for orthotic and prosthetics, and supplies

-

Physicians and non-physician practitioners if the DMEPOS items are furnished only to his or her patients as part of his or her professional services

-

Physical and occupation therapists if: (1) the business is solely-owned and operated by the therapist, and (2) if the DMEPOS items are furnished only to his or her patients as part of his or her professional service.

Goldleaf Surety has a number of good surety markets that write Medicare bonds or DMEPOS. For DMEPOS - or all types of bonds - you can contact Goldleaf Surety through Big "I" Markets.

|

Big "I" Flood partner Selective knows writing flood insurance business is complex - and agents already have a lot on their plate, so any time saved means more time for them to capture new business. Big "I" Flood partner Selective knows writing flood insurance business is complex - and agents already have a lot on their plate, so any time saved means more time for them to capture new business.

For this reason, Selective offers QuoteitNow - a self-service flood quoting tool that can be easily added to Selective appointed agency Web sites. In just a few simple steps, QuoteitNow walks customers through a flood application up to binding and directs them to contact the agency to finalize the process.

Why not maintain a personal touch with customers, while empowering them to start the flood quote process on their own - and at their convenience? Work with Selective to save time, save money and drive business. To learn more watch a brief overview video here. For additional questions or to become a Selective appointed flood agent, contact Quoteitnow@selective.com or visit www.iiaba.net/Flood.

Last week's version of this story mistakenly mentioned state exclusions. QuoteitNow is currently available nationwide.

|

By Michael Welch, Big "I" Advantage Marketing Assistant

Thanksgiving is a time to gather together and give thanks for all the bounty in our lives. A day steeped in tradition, it is a time of love, peace, family and football. What could compare to a house full of family and friends around a meal that can last half a day? Despite your best efforts to keep the peace, some disagreements may break out. Especially when it comes to food! Check out our lineup of famous Thanksgiving food fault lines. Thanksgiving is a time to gather together and give thanks for all the bounty in our lives. A day steeped in tradition, it is a time of love, peace, family and football. What could compare to a house full of family and friends around a meal that can last half a day? Despite your best efforts to keep the peace, some disagreements may break out. Especially when it comes to food! Check out our lineup of famous Thanksgiving food fault lines.

Turkey: Roasted vs. Smoked vs. Fried

Some people will argue a certain cooking method is best. Traditional methods compete with the new-fangled deep-fryer. While I've had all three and find them all delicious, my only contribution is that I found fried turkey to be moister the following day. Additionally the E&O folks would probably insist I add that if you do fry a turkey take extra precautions. Who better than Captain Kirk (with a little help from State Farm) to show you how not to fry a turkey? Alton Brown can show you how to fry without mishap. Lastly here is a trick from Butterball to get a roasted turkey out easily.

Turkey vs. Ham vs. Seafood

Turkey is the traditional main course. Ham is usually reserved for Christmas but sometimes they get flipped or the same is served for both. The original Thanksgiving may or may not have included a turkey or two, but it definitely had fish and shellfish, including mussels, oysters and clams. Depending on the number of guests a combination of all three could be served.

Dressing vs. Stuffing: Which is Which?

The confusion probably stems from the fact that the recipes for either can be the same. Some people say dressing is stuffing only if cooked in the bird. Others say the terms are interchangeable. Since there are health risks if the stuffing is not brought up to a proper temperature some cooks pull the stuffing out when the bird is done or nearly so and then finish the off in the oven. All that and you still have the prepared vs. homemade toasted/cubed bread disagreement with which to contend.

Cranberry Sauce

A great debate rages over the fresh taste of homemade versus the nostalgia of canned. On one hand there are probably a million different ways to prepare cranberries, hot and cold. My own recipe can be found at the bottom of this article. Canned devotees love the back-to-childhood memories they get and also swear the ridges left by the can give a textural feel that homemade can't match.

Pies: Pecan vs. Pumpkin vs. Sweet Potato vs. Fruit vs. Mincemeat

Apple pie is the perennial favorite with pumpkin, chocolate, cherry, and pecan jockeying for position. The fight over which is "best" is probably why lots of families will have at least two or three varieties. Some like it served hot, other prefer room temperature or even refrigerated. You've also got to have whipped cream and ice cream for people to top their slices.

While perhaps not quite as contentious, the following can still cause some grumbling:

Green Beans vs. Green Bean Casserole

Mac-n-Cheese (Baked or not) vs. Potatoes au Gratin

Corn Pudding vs. Roasted Corn

Homemade Rolls vs. Packaged Rolls

Lastly - please click here to enjoy a few favorite recipes collected from your Big “I” association staff.

May your Thanksgiving be happy, healthy and safe. Best wishes from all of us at Big "I" Markets.

|

| |

Remember that you can view the following webinars 24/7 by checking out the BIM Webinar Library. To do that log onto Big "I" Markets and click on "Publications".

-

AIG Private Client Group Homeowner - Overview NEW

-

TravPay

-

Commercial Lessor's Risk

-

Affluent Homeowners

-

Travel Insurance

-

Community Banks

-

Affluent Homeowner

-

Real Estate E&O

-

RLI Personal Umbrella

-

"Oh, by the way...Flood Sale"

-

Habitational

-

Student Housing

+++++

BIM WEBSITE TRAINING WEBINAR

For all you folks who recently registered for Big "I" Markets, remember you can participate in a webinar from the comfort of your office to help you learn how to navigate around the system. Every Thursday at 2:00 p.m. EDT we'll show you how to navigate the Big "I" Markets platform, including how to submit a quote! A recording of this webinar can be found under "Publications" after logging into Big "I" Markets.

+++++

Big "I" Markets Product Webinars

Wednesday, December 7 - 2:00 - 2:30pm EST. AIG Private Client Group for affluent homeowners. This webinar will cover what qualifies as a collectible car, (classic, antique, exotic, etc.) plus the features of their Automobile coverage.

-

New Vehicle Replacement

-

High Liability Limits

-

Worldwide Coverage

-

OEM Parts

-

Cash Settlement Option

-

...and more

Click here to register.

+++++

Learn Your Agency Web Site Liability Risks

The Big "I" Professional Liability/Swiss Re Corporate Solutions quarterly risk management webinar has been set for December 8, 2016 at 2 P.M. EDT. "Agency Risk Management Essentials: Is your website doing more harm than good?" will focus on the risks associated with insurance agency Web site content. The discussion will be presented from the viewpoints of an agents E&O underwriter, an auditor, a claims specialist and defense counsel and will include dos and don'ts when it comes to web site content.

Panelists will include senior Swiss Re Corporate Solutions staff, and the session will be moderated by IIABA's Jim Hanley, RPLU, Director Agency Professional Liability Risk Management.

Big "I" Professional Liability welcomes suggested questions related to the topic for discussion during the session. Please email Jim Hanley no later than November 30th with your thoughts.

Register for the complimentary session today. No Continuing Education credits are offered for this webinar.

+++++

Big "I" Virtual University Webinars

Don't miss the following education opportunities provided from the Big "I" Virtual University experts that focus on topics agents need to know to make a smart start in 2016. For more information, contact national staff.

-

December 5 - 2:00 - 2:30pm EST. "First Monday LIVE!" is a free monthly webcast hosted by the VU's own Bill Wilson and guests on the first Monday of the month to discuss the wide world of insurance from seemingly non-insurance topics. Each 30-minute webisode covers "what's going on" in the news and the implications. The December broadcast is in development as subject matter is explored. Click here to learn more and register and here to access the recordings.

-

December 7 - 1:00 - 2:00pm EST. "What I've Learned in 47 Years In the Insurance Industry". A free webinar with parting thoughts from Bill Wilson who is retiring at the end of 2016 and whose career began in June 1969 when he graduated from high school and worked during the summer for the industry organization that had granted him a 4-year scholarship to college, majoring in fire protection engineering. Over the next 47 years, his career morphed from engineering to management to education, serving largely insurance carriers then independent insurance agents. Over the time, he's learned a few things you might find helpful. Click here to register.

|

STUDENT OF THE INDUSTRY PARTING SHOT

Bitcoins and Insurance

Excuse me, say that again?

By Paul Buse, President of Big I Advantage®

I was on a teleconference recently with our regulator of captive insurers in the District of Columbia, Dana Sheppard. During the call Bitcoin was mentioned with respect to captive insurers. My reaction was a chin rub and a muttering of, "Hmmm…interesting…" and, then, a raised eye-brow as I wondered if perhaps marijuana was involved. That pondering aside, it might be that Bitcoin is getting ready to move in on Insurance Street.

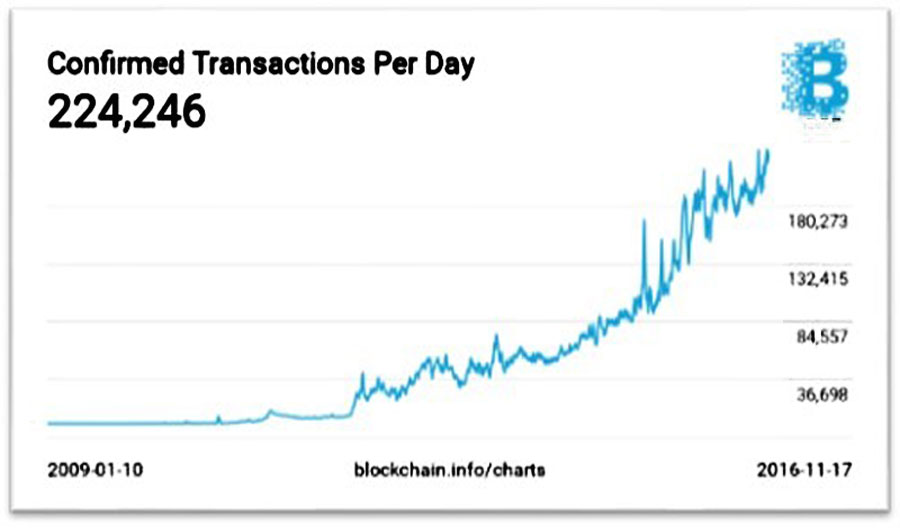

Click for larger version

Source: Blockchaininfo.org

Now, if the concept of insurance and Bitcoin is totally unfamiliar to you, you are not alone. You are like me only a few months ago. As students, we may want to keep watch because experts indicate Bitcoin and insurance is here.

I feel like we are at the point where the Internet was at the "World Wide Wait" stage and many were skeptical it would have any impact on insurance. Remember that, right after Y2K? Some are calling Bitcoin and its related processes called Block Chain "Internet 2.0." That is, Internet 1.0 was the exchange of information. Internet 2.0 will be the same sort of revolution in the exchange of monetary value. Just like Internet 1.0 though…no one knows for sure.

What is Bitcoin? In a nutshell, Bitcoin is a form of digital currency, created and held electronically. Diving much deeper into what, where, how, etc. defies the remaining space here but after my research, I suggest you first consider what it portends to do and leave the details of how for some self-research at a later date at Bitcoin.org or Blockchain.info.

So what does Bitcoin/Block Chain portend to do? It will allow the exchange of value from person to business, business to business or, in our case and what is happening already, reinsurer to insurer, outside of the traditional bank clearing system: Payer to collector.

Do you know any insurance Bitcoin stories? Write me at paul.buse@iiaba.net. The one I'm curious about after that teleconference is nascent marijuana businesses and their potential use of insurers that pay claims in Bitcoin.

|

BIG "I" MARKETS SALE OF THE WEEK

Congratulations to our agent in Utah on a surety bond sale of $12,900 in premium!

|

|